Health Savings Accounts (HSAs) are a popular way to save money for medical expenses thanks to their unique tax advantages. But when it comes to your children, things can get a bit tricky. Can you use your HSA funds to pay for your child’s medical costs?

The short answer is yes—but only under certain conditions. Understanding HSA rules, dependent qualifications, and tax implications is key to using these funds properly. Let’s explore this topic in a clear and simple way.

Using Your HSA for Your Child’s Medical Expenses

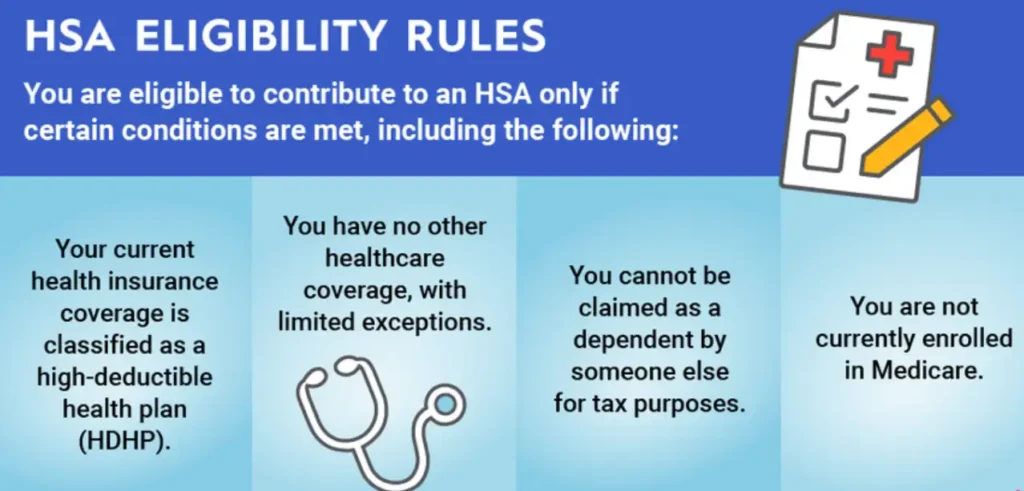

HSAs are designed to cover qualified medical expenses tax-free. You can use these funds for yourself, your spouse, and anyone you claim as a dependent on your tax return.

This means that if your child qualifies as a tax dependent, you can use your HSA to pay for their medical costs, even if they are not covered under your health insurance plan.

For many parents, this is a helpful way to manage healthcare expenses without dipping into other savings.

However, not every child qualifies. The IRS has strict guidelines for who counts as a dependent, and failing to meet these rules can lead to penalties.

For example, if you use your HSA for a child who does not meet dependency qualifications, the withdrawn amount becomes taxable income, and you’ll face an additional 20% penalty if you’re under 65. This is why it’s crucial to understand whether your child fits the IRS criteria.

How Does the IRS Define a Dependent?

To use your HSA for your child’s expenses, they must meet the IRS definition of a dependent. The general criteria include the following:

- Your child must be under the age of 19, or under 24 if they are a full-time student.

- You must provide more than half of their financial support for the year.

- They must live with you for more than half the year, except in cases like temporary absences for education or medical care.

For children who meet these conditions, their medical expenses are eligible for tax-free withdrawals from your HSA. This rule applies even if your child is not covered under your high-deductible health plan (HDHP), which is often a point of confusion for many parents.

What About Adult Children?

Things get a bit more complicated when it comes to adult children. If your child is over the age of 24 or no longer meets the IRS dependency criteria, you cannot use your HSA to pay for their medical costs.

Even if you want to help cover their expenses, doing so with your HSA funds would trigger tax consequences.

The withdrawn amount would be considered taxable income, and if you’re under 65, you’d also face a 20% penalty.

At this stage, it’s better for adult children to open their own HSAs if they qualify. To be eligible, they must have their own high-deductible health plan (HDHP) and no other disqualifying coverage.

An HSA is a smart way for young adults to manage healthcare costs while also saving for the future.

How HSAs Work After You Turn 65

Once you reach age 65, HSA rules change slightly. At this point, you can withdraw HSA funds for any purpose without facing the 20% penalty.

However, if you use the money for non-medical expenses, it will be treated as taxable income, similar to withdrawals from a traditional IRA.

For qualified medical expenses, though, the tax-free benefits of your HSA remain intact. This flexibility can make HSAs an even more valuable financial tool in retirement.

Final Thoughts

Using your HSA to pay for your child’s medical expenses can be a smart and tax-efficient move—as long as your child qualifies as a dependent under IRS rules.

If you’re unsure about your child’s status or the expenses you plan to cover, it’s always a good idea to consult a tax professional.

Misusing HSA funds can lead to unexpected taxes and penalties, which defeats the purpose of this powerful savings tool.

By understanding the rules and keeping careful records, you can make the most of your HSA while ensuring your family’s healthcare needs are covered.

Whether you’re paying for routine checkups, prescriptions, or unexpected medical bills, an HSA can provide valuable financial relief when used correctly.